Your sales reps attended the training. They passed the assessment. They know your products, your pitch, and your battle cards. And then a customer pushes back with a comparison to a competitor, a borrower raises common objections on a collections call, or an HNI client says, “I’m already covered”; and the conversation falls apart.

The gap between knowing and doing is where most enterprise sales revenue goes to die. AI sales training tells sales professionals what good looks like. But AI sales role play and realistic role play simulations help them apply those skills under pressure, in real life, with customers who never follow a script. For sales management and sales leaders, this is the difference between one-time training and continuous improvement that delivers long term performance gains.

The best sales role play scenarios close that gap because they reflect the actual conversations your sales representatives have every day. Generic role playing scenarios or a basic training tool cannot prepare an insurance advisor for an IRDAI compliance objection. A US-built cold-calling simulation will not prepare your branch RM for a guarded, first-generation banking customer in a Tier-2 city. The most effective AI sales role play platform recreates these high-stakes conversations, giving reps safe, repeatable practice before they face customers.

This guide covers the 10 most impactful AI sales roleplay scenarios for enterprise teams in 2026; built around Disprz’s core ICP verticals: banking, insurance, pharma, retail, automotive dealerships, financial services, and IT services. Each scenario includes India-specific variants where the dynamics differ meaningfully from global norms. If you’re new to AI sales coaching and want context on how these scenarios fit into a broader coaching system, our complete guide to AI sales coaching is the right place to start.

For each scenario, you’ll find: the business case for practising it, the buyer persona to build, the three skill moments the AI should score, what good looks like, and what a common failure pattern looks like. Use these as briefs to configure your own scenarios in any AI sales roleplay platform; or in Disprz Sales Coach directly.

Why Scenario Practice Beats Training Alone

The learning science behind scenario-based practice is unambiguous. According to Allego’s 2025 research, 43% of revenue enablement leaders now use AI-powered roleplay to enhance sales coaching; and teams using AI coaching are 20% more likely to improve revenue outcomes compared with those that don’t.

The reason is simple: skills are built through retrieval and application, not passive consumption. A rep who reads a battle card knows what’s on it. A rep who has practiced handling a price objection from a hesitant car buyer in 50 simulated conversations knows how to do it under pressure, when the customer pushes back and the script no longer applies.

That’s what each of the scenarios below is designed to produce: not knowledge, but capability. Not recall, but instinct.

What Makes a Great AI Roleplay Scenario?

Before the 10 scenarios, a quick framework. A high-quality AI sales roleplay scenario has five components:

- A specific, realistic customer persona. Name, role or background, emotional state at the start of the call, prior experience with your brand or category, and a defined decision style. “A hesitant customer” is not a persona. “Meena Iyer, 38, schoolteacher, six-year banking relationship, slightly wary of ‘schemes’ after a colleague had a bad experience”; that’s a persona.

- A clear call objective. What does success look like for the rep at the end of this conversation? Not “make the sale”; but “secure a follow-up appointment to discuss a child education plan” or “secure a dated, specific repayment commitment.” Specific outcomes drive specific behaviours.

- Defined scoring moments. Three to five specific conversation behaviours the AI should evaluate: did the rep ask a qualifying question in the first 90 seconds? Did they acknowledge the objection before countering it? Did they advance to a clear next step before ending the call?

- A realistic objection or pressure point. Without a real challenge, the rep isn’t practising; they’re performing. Every scenario needs at least one moment that requires the rep to think, adapt, and recover.

- A post-session debrief structure. What should the rep reflect on? What does the scorecard show? Where is the benchmark for “good” in this scenario?

With that frame in place; here are the 10 scenarios:

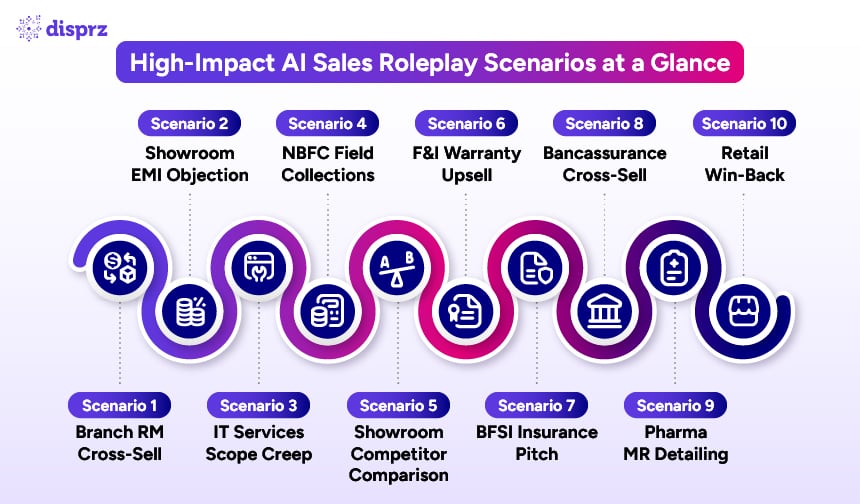

Scenario 1: Branch RM Cross-Selling to a Hesitant Retail Customer

The Business Case

Cross-selling is how banks grow wallet share without acquiring new customers; but it’s also where trust breaks down fastest. A relationship manager who pushes a product too early reads as a salesperson, not an advisor, and the customer disengages from the entire branch relationship, not just that product. Most RM training covers product features. Almost none of it trains the actual conversation: how to introduce a relevant product without making the customer feel sold to.

The Persona

Customer: Meena Iyer, 38, schoolteacher, has held a savings account at the branch for six years. She came in today to update her KYC documents; nothing more. She has no active investments beyond a recurring deposit. She’s mildly wary of ‘bank schemes’ after a colleague was sold a product she didn’t understand. Emotional state: neutral, slightly guarded if the conversation shifts from her stated purpose.

The Three Scoring Moments

- Earning permission to go beyond the stated purpose (first 60 seconds): Did the RM complete Meena’s actual request first and ask permission before introducing anything else (‘while you’re here, may I ask about something else?’) rather than pivoting straight into a product pitch?

- Need discovery before product mention: Did the RM ask about Meena’s financial goals or upcoming life events (her daughter’s education, a planned home purchase) before naming any specific product? Or did they lead with ‘we have a great mutual fund scheme right now’?

- Handling ‘I need to think about it’: When Meena hesitates, did the RM acknowledge the hesitation respectfully and offer a low-commitment next step (a follow-up call, a one-page comparison); or did they apply pressure to decide on the spot?

What Good Looks Like

“Meena ma’am, your KYC update is done. Before you go; would it be alright if I ask one quick question, unrelated to today’s visit? You mentioned your daughter is in Class 9 now; have you started planning for her higher education costs?”

What Failure Looks Like

“Meena ma’am, since you’re here; we have an excellent ULIP scheme running right now with great returns, would you like to hear about it?” Meena’s guard goes up immediately and she ends the conversation as quickly as possible.

India Context

PSU bank variant: customers at PSU bank branches in Tier-2 and Tier-3 cities are often first-generation banking customers with lower financial literacy and higher trust sensitivity. Build a Hindi-language variant of this scenario where the RM must explain concepts like SIP or term insurance in plain language without sounding patronising; a skill rarely covered in product training.

Scenario 2: Showroom Sales Executive Handling a Price / EMI Objection

The Business Case

The single most common moment a car deal is lost is the price objection; and the most common reason it’s lost badly is that the sales executive jumps straight to a discount instead of understanding what’s actually driving the hesitation. In dealership groups, where margins on the vehicle itself are thin and the real profitability sits in financing, accessories, and after-sales, an executive who discounts reflexively is giving away the dealership’s actual margin to solve a problem that may not even be about price.

The Persona

Customer: Vikas Choudhary, 34, IT professional, has test-driven the vehicle twice and is clearly interested. He says the on-road price is ‘more than I budgeted for’ and mentions a competing dealership quoted a lower price on a similar model. He hasn’t discussed financing in detail yet. Emotional state: genuinely interested but anchored on a number, slightly testing whether the executive will fold.

The Three Scoring Moments

- Diagnosing before discounting: Did the executive ask what specifically feels over-budget (the on-road price, the EMI, or the down payment) before offering any reduction? Most customers are reacting to the EMI, not the sticker price, and the conversation changes entirely once that’s clear.

- Responding to the competitor quote: When Vikas mentions a lower quote elsewhere, did the executive ask what exactly was included (accessories, extended warranty, exchange bonus) before reacting to the number; or did they immediately offer to match it?

- Reframing around total value, not price: Did the executive walk Vikas through financing structure, exchange value, and after-sales package as a complete value picture; rather than simply lowering the quoted price to close the gap?

What Good Looks Like

“Vikas, help me understand; when you say it’s more than budgeted, is it the total on-road price, or is it more about the monthly EMI number? Because those are two different problems, and they have different solutions.”

What Failure Looks Like

“Okay sir, let me see what discount I can get approved for you”; within the first minute of the objection, before understanding whether Vikas even needs a discount or simply needs a different financing structure.

Scenario 3: IT Services Account Manager Handling Scope Creep on a Live Project

The Business Case

Scope creep conversations are where IT services account managers either protect their delivery margin or quietly erode it. The client side of the table usually has multiple stakeholders with different agendas; a delivery sponsor who wants the extra work done quietly, a procurement contact who won’t approve a change order, and a business user who just wants their problem solved and doesn’t care how it gets billed. An account manager who can’t read the room ends up either damaging the relationship by refusing everything, or absorbing unbilled work that quietly destroys account profitability.

The Persona (Three Simultaneous Client Stakeholders)

- Kavita Subramaniam, Client VP of Operations: The business sponsor. She wants the additional reporting feature built; her team needs it for a board presentation in three weeks. She assumes it’s a small task and doesn’t see why it would cost extra.

- Rohan Desai, Client Procurement Lead: Focused on contract terms. He won’t approve any change order without a clear scope document and will push back hard on anything that looks like a new SOW disguised as a minor change.

- Arjun Bhatt, Client IT Manager: The day-to-day contact who raised the request informally over email, without realising it would trigger a formal change process. He’s caught in the middle and slightly embarrassed.

The Three Scoring Moments

- Naming the scope change without blame: Did the account manager acknowledge the request as reasonable while clearly stating it falls outside the current SOW; without making Arjun feel like he did something wrong by asking?

- Aligning the room before quoting a number: Did the account manager check whether Kavita and Rohan were aligned on priority and budget before presenting a cost and timeline; or did they quote a number to whoever asked first, creating internal client friction?

- Protecting the relationship while protecting margin: Did the account manager offer a path forward (a scoped change order, a phased approach) rather than a flat ‘yes’ that erodes margin or a flat ‘no’ that damages the relationship?

What Good Looks Like

“Arjun, this is a completely fair task, and I understand the board deadline makes it feel urgent. Here’s where it sits, though; this wasn’t part of the original scope, so before I can commit a timeline, I need Rohan and Kavita aligned on priority and budget. Can the three of us get 15 minutes today?”

What Failure Looks Like

The account manager tells Arjun “sure, we’ll just fit it in” to avoid an awkward conversation; and three more ‘small asks’ follow over the next month, none of them billed, all of them eating into the delivery team’s bandwidth.

Scenario 4: NBFC Field Collections Agent Negotiating with a Stressed Borrower

The Business Case

Collections is one of the most emotionally demanding conversations in financial services; and one of the least practiced. An agent who treats every borrower the same way, with the same script, either escalates a recoverable situation into a complaint and reputational risk, or fails to firmly secure a repayment commitment from a borrower who could pay but is stalling. The skill isn’t persistence. It’s reading whether the borrower genuinely can’t pay, won’t pay, or simply hasn’t been asked the right way.

The Persona

Borrower: Suresh Yadav, 41, runs a small hardware shop, has missed two EMI payments on a business loan after a slow festive season. He’s not avoiding the call; he picks up; but he’s defensive and slightly embarrassed. He has partial capacity to pay this month but not the full amount. Emotional state: stressed, guarded, sensitive to any tone that feels like a threat.

The Three Scoring Moments

- Opening without escalating: Did the agent open the call in a tone that invites a conversation rather than announcing a default; acknowledging the relationship and asking what’s going on, rather than leading with the overdue amount and a warning?

- Diagnosing capacity, not just intent: Did the agent ask specific questions to understand whether Suresh can pay something now versus needing a revised schedule; rather than pushing for the full amount regardless of what he says he can manage?

- Securing a specific, realistic commitment: Did the call end with a concrete, dated commitment (‘₹8,000 by Friday, remainder restructured over two months’) rather than a vague ‘I’ll try to pay soon’ that both sides know won’t hold?

What Good Looks Like

“Suresh ji, I can see you’ve been a regular payer until the last two months; something’s clearly changed. Tell me what’s going on with the shop right now, and let’s see what we can work out together.”

What Failure Looks Like

“Sir, your account is now 45 days overdue and this will be reported. I need the full payment today.” Suresh becomes defensive, the call ends without any commitment, and the relationship is now adversarial for every future contact.

India Context

This scenario is highly sensitive to tone and language. Build Hindi and regional-language variants for field collections teams, and calibrate the AI borrower’s emotional escalation carefully; the training goal is de-escalation and empathy, not aggressive recovery tactics.

Scenario 5: Showroom Executive Handling a Competitor Model Comparison

The Business Case

Almost every car buyer test-drives at more than one dealership before deciding. ‘I also test-drove the [competitor model] and it had better mileage’ is one of the most common moments in automotive retail; and one of the most poorly handled. Executives either get defensive about their own brand or concede the comparison entirely and let price become the only differentiator left.

The Persona

Customer: Priya Bansal, 29, first-time car buyer, has test-driven both this model and a closely-priced competitor SUV. She read the competitor’s mileage figures online and is using them as her primary comparison point. She’s engaged and asking genuine questions; not hostile, but she expects an honest, specific answer, not a dismissal of the competitor.

The Three Scoring Moments

- Acknowledging the competitor’s claim accurately: Did the executive confirm or correctly contextualise the competitor’s mileage figure rather than disputing it without evidence; which would immediately damage credibility with an informed buyer?

- Reframing around Priya’s actual use case: Did the executive ask about Priya’s typical driving pattern (city commute vs. highway, family size, parking constraints) and connect the comparison to her specific situation; rather than reciting a generic feature list?

- Closing the gap with total ownership value: Did the executive bring in service network density, resale value, and warranty terms as part of the comparison; building a complete picture rather than leaving mileage as the only variable in Priya’s mind?

What Good Looks Like

“Priya, that mileage figure is accurate for highway driving; in city conditions, the gap narrows quite a bit. Can I ask, is most of your driving going to be the daily office commute, or are you also doing longer highway trips on weekends? That actually changes which of the two makes more sense for you.”

What Failure Looks Like

“That figure isn’t accurate, our model is actually more efficient”; stated without evidence, to a buyer who has already done her own research and now trusts the executive less.

Scenario 6: F&I Manager Upselling Extended Warranty at Vehicle Delivery

The Business Case

The finance and insurance (F&I) conversation at delivery is one of the highest-margin moments in automotive retail; and one of the easiest to get wrong. The customer has already committed to the vehicle and is excited to take delivery. An F&I manager who pushes too hard at this moment creates buyer’s remorse that shows up in post-sale satisfaction scores and referral willingness. One who doesn’t raise the conversation at all leaves margin on the table that the dealership group depends on.

The Persona

Customer: Rohit Verma, 45, business owner, taking delivery of his new SUV today with his family present. He’s in a good mood and ready to leave with the keys. He has not previously discussed extended warranty or accessories. Emotional state: happy, slightly impatient to finish paperwork and drive away.

The Three Scoring Moments

- Reading the moment before pitching: Did the F&I manager acknowledge Rohit’s excitement and keep the interaction brief and respectful of his time, rather than launching into a long product presentation that delays delivery?

- Framing around risk, not features: Did the manager connect the extended warranty to something Rohit would actually care about; protecting a family vehicle, avoiding unexpected repair costs; rather than reciting coverage terms and conditions?

- Respecting a decline gracefully: If Rohit declines, did the manager accept it without a second or third push, and close the interaction warmly; protecting the overall delivery experience rather than the upsell?

What Good Looks Like

“Rohit, congratulations again; I won’t hold you up. One thing worth 30 seconds: since this is a family vehicle, a lot of our customers extend the warranty just for peace of mind on unexpected repairs. Want me to quickly show you what it covers, or would you rather we just get you on the road?”

What Failure Looks Like

The F&I manager spends 15 minutes on a detailed warranty presentation while Rohit’s family waits in the car, visibly impatient; and Rohit leaves the dealership frustrated despite buying the vehicle he wanted.

Scenario 7: BFSI Insurance Product Pitch (India)

The Business Case

India’s insurance sector has the largest frontline sales workforce in the world; and one of the highest-stakes sales conversations in any category. Agents must demonstrate product knowledge, regulatory awareness, and empathy simultaneously. IRDAI pre-licensing mandates require demonstrable competence before agents go live. A failed pitch from an under-prepared agent doesn’t just lose the sale; it creates mis-selling risk and potential regulatory liability.

The Persona

Buyer: Lakshmi Iyer, 52, school principal from Chennai. Moderate savings. She’s been approached by agents before and had a bad experience; she was sold an ULIP she didn’t understand and had to surrender it at a loss. She’s now cautious. She’s considering a pure term plan for her family’s protection. Emotional state: guarded, needs to feel respected and understood, not sold to.

The Three Scoring Moments

- Needs-based selling vs product pushing: Did the rep ask about Lakshmi’s family situation and financial goals before presenting any product? Did they lead with her context or their premium?

- Explaining the product clearly: When Lakshmi asks “But what happens if I survive the term?”; a classic term insurance objection; did the rep explain the logic of pure protection calmly and clearly, without making her feel foolish for asking?

- Compliance guardrails: Did the rep disclose appropriately (no guaranteed return claims, no misleading comparisons to FDs)? This is scored for IRDAI compliance alignment.

What Good Looks Like

“Lakshmi ji, before I tell you about any product; can I ask: what worries you most when you think about your family’s financial security? Not what you’ve already planned for; what still keeps you up at night?” The rep listens to the full answer before speaking again.

India Context

India-specific scoring: Add an IRDAI compliance sub-score to this scenario. The AI flags any claim that violates IRDA’s regulations on guaranteed returns, mis-selling, or misleading comparison. Failing this sub-score is a training escalation trigger, not just a coaching point.

Scenario 8: Bancassurance Cross-Sell to an HNI Client (India)

The Business Case

Bancassurance cross-sell is one of the highest-value and highest-risk conversations a bank RM has. Bringing an insurance product into an existing banking relationship requires the RM to introduce something new without appearing to change the nature of the relationship. Pushed too hard, the client feels sold to and reduces their banking relationship. Done well, it deepens trust and expands wallet share.

The Persona

Buyer: Vikram Malhotra, 47, entrepreneur in Delhi-NCR. HNI client with a long-standing relationship with the bank (8+ years). He trusts his RM personally. He has existing investments and is not actively looking for insurance. His business has been doing well. He’s time-poor and skeptical of anything that feels like a sales pitch from his bank.

The Three Scoring Moments

- Transition without the switch: Did the rep introduce the insurance conversation as a natural extension of a broader financial planning discussion; not as ‘I also wanted to share something with you today’?

- Leading with Vikram’s situation, not the product: Did the rep reference something specific about Vikram’s business or financial situation (something the RM would actually know) before introducing any product?

- Handling ‘I’m already covered’: When Vikram says he has an existing life cover, did the rep ask a curious question about whether the coverage still reflects his current business exposure; rather than immediately countering with a product pitch?

What Good Looks Like

“Vikram bhai, your business has grown significantly in the last two years. A lot of our clients in similar positions find that their original life cover (taken when the business was smaller) no longer matches their current liability profile. I’m not assuming that’s true for you, but it might be worth a five-minute conversation to check. Would that be useful?”

India Context

Variants: Build this scenario in Hindi for Tier-2 city RMs. The language formality, the appropriate use of honorifics, and the pacing of a conversation with an HNI client differ significantly from English-language training materials. Vernacular AI personas are a differentiated capability that no US-based roleplay tool can replicate at this fidelity.

Scenario 9: Pharma MR Detailing to a Sceptical HCP (India)

The Business Case

India has one of the world’s largest medical representative workforces; over 600,000 MRs operating across hospitals, clinics, and chemist networks. MR detailing is among the most demanding sales conversations in any industry: the buyer (a doctor or pharmacist) has domain expertise that exceeds the seller’s, the time window is typically under three minutes, and any clinical overreach can damage the company’s credibility permanently.

The Persona

Buyer: Dr. Rajeev Nair, Senior Cardiologist at a 300-bed private hospital in Kochi. He sees 12–15 MR visits per week and has seen every pitch. He is genuinely time-poor. He’s particularly sceptical of any claim that isn’t backed by a peer-reviewed RCT. He finds most MR visits a waste of his time; but he will engage with a rep who demonstrates real clinical knowledge and respects his time.

The Three Scoring Moments

- Opening with clinical relevance: Did the rep lead with a specific clinical insight relevant to Dr. Nair’s patient population rather than a product benefit? Did they reference a specific study or patient profile?

- Handling the evidence challenge: When Dr. Nair says “the ATLAS trial data on this class of drug is mixed; why should I trust your study?” did the rep engage with the specific concern credibly, or deflect?

- Respecting the three-minute boundary: Did the rep read the signal when Dr. Nair’s attention shifted, close the detailing crisply, and leave a clear next step (a dinner symposium, a journal reprint) rather than trying to extend the call?

What Good Looks Like

“Dr. Nair, I have three minutes and I want to use them well. There’s a sub-group analysis from the Phase 3 trial that’s specifically relevant to your hypertensive heart failure patients; the ones who aren’t responding to the standard ACE inhibitor protocol. Can I show you that one slide?”

Scenario 10: Retail Store Associate Winning Back a Dissatisfied Customer

The Business Case

A customer who had a bad experience and stopped shopping at a store represents one of the highest-value conversations in retail; they already know the brand, the location, and the product range. Winning them back costs a fraction of acquiring a new customer. But the conversation requires genuine acknowledgement of what went wrong, not a generic apology followed immediately by a new pitch. Most frontline staff have never been trained for this conversation specifically; only for new-customer service.

The Persona

Customer: Ananya Krishnamurthy, a longtime customer who stopped shopping at this store six months ago after a poor experience; a defective product exchange that took three visits and multiple unclear explanations to resolve. She’s back in the store today browsing, not actively looking to engage with staff, somewhat guarded if approached. Emotional state: mildly resentful, testing whether anything has actually changed.

The Three Scoring Moments

- Recognising and acknowledging, not assuming: If the associate recognises Ananya as a lapsed customer, did they acknowledge the gap respectfully (‘it’s been a while, welcome back’) without putting her on the spot or making her explain why she stopped visiting?

- Addressing past issues if raised, specifically: If Ananya mentions the past bad experience, did the associate listen fully and acknowledge the specific failure, rather than offering a generic ‘sorry about that’ and changing the subject?

- Rebuilding trust through action, not promises: Did the associate offer something concrete and low-risk; walking her through the current exchange policy, offering to personally handle any future issue; rather than simply asserting that ‘things have improved’?

What Good Looks Like

“Ananya ji, it’s good to see you again; it’s been a while. If you don’t mind me asking, I remember there was some difficulty with an exchange last time. We’ve actually changed that process since then; would it help if I walked you through how it works now, so you know what to expect if you ever need it?”

What Failure Looks Like

“Welcome back! Have you seen our new collection?”; ignoring the prior bad experience entirely and pivoting straight to a sale, leaving Ananya feeling like nothing has actually changed.

At-a-Glance: All 10 Scenarios

Use this summary table to prioritise which scenarios to build first based on your team’s current development priorities.

| Scenario | Skill Trained | Customer Persona | Difficulty | India Variant? |

|---|---|---|---|---|

| Branch RM Cross-Sell | Trust-building, soft cross-sell | Long-standing bank customer | Beginner | Yes; PSU bank, Hindi |

| Showroom EMI Objection | Value defence, financing literacy | First-time car buyer | Intermediate | N/A |

| IT Services Scope Creep | Reading the room, margin protection | Client VP + Procurement + IT Manager | Advanced | N/A |

| NBFC Field Collections | Empathy under pressure, negotiation | Stressed small-business borrower | Intermediate | Yes; vernacular |

| Showroom Competitor Comparison | Differentiation, objection reframing | Informed first-time buyer | Advanced | N/A |

| F&I Warranty Upsell | Value-based upsell, timing | Customer at vehicle delivery | Intermediate | N/A |

| BFSI Insurance Pitch | Compliance + trust | India insurance buyer | Intermediate | Yes; core scenario |

| Bancassurance Cross-Sell | Cross-sell without push | HNI retail banking client | Advanced | Yes; core scenario |

| Pharma MR Detailing | Clinical credibility | Sceptical HCP | Advanced | N/A |

| Retail Win-Back | Re-engagement, rebuilding trust | Dissatisfied lapsed customer | Advanced | N/A |

For most enterprise teams in Disprz’s core verticals, Scenarios 1 (Branch RM Cross-Sell), 2 (Showroom EMI Objection), and 7 (BFSI Insurance Pitch) deliver the highest return per hour of practice time. If you’re building a sales coaching programme from scratch, these three are the place to start.

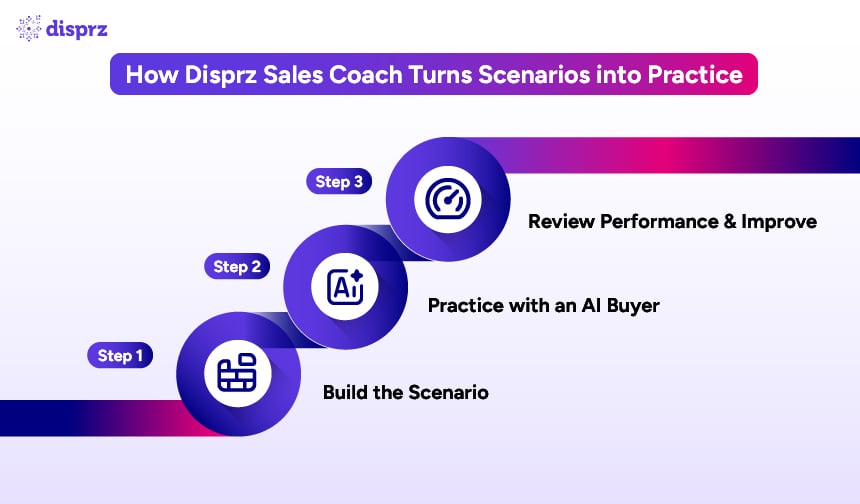

How to Run These Scenarios in Disprz Sales Coach

Every scenario above can be configured in Disprz Sales Coach in under 30 minutes. Here’s how the three-step workflow maps to the briefs above:

- Step 1 (Build the Scenario): Enter the buyer persona details: name, role, seniority, emotional state, prior product knowledge, decision style. Paste in the scenario brief as the situation description. Set the call objective as the scoring target. Upload any product decks, battle cards, or SOPs you want the AI buyer to reference.

- Step 2 (Practice the Roleplay): The rep enters a voice-based, two-way conversation. The AI buyer adapts dynamically to the rep’s responses; including deploying the objections and pressure points described in each scenario briefly above. No scripts, no safety net.

- Step 3 (Review the Scorecard): Post-session analytics identify every scored moment: talk ratio, filler words, deal-stage progression, and the three specific scoring behaviours defined for each scenario. The rep receives a personalized action plan. The manager sees a team-level dashboard.

For India-specific scenarios (7, 8, 9), Disprz Sales Coach supports vernacular persona configurations and industry-specific scoring rubrics; including IRDAI compliance sub-scores for insurance agent training and RBI-aligned objection profiles for banking collections teams. These are not available in US-built roleplay platforms that default to Western sales culture personas.

Key Takeaways

- Scenario specificity is everything. A generic ‘sales call’ roleplay does not prepare a rep for a procurement negotiation or a BFSI insurance pitch. The persona, the pressure point, and the scoring moments must be designed for the specific conversation the rep will actually have.

- India enterprise teams need India scenarios. BFSI, insurance, and pharma sales in India involve regulatory requirements, cultural dynamics, and buyer psychology that US-built training materials don’t address. Scenarios 7, 8, and 9 are built specifically for these contexts.

- Three scoring moments per scenario is the right design target. More than five becomes overwhelming; fewer than three doesn’t capture the conversation arc. Each moment should map to a specific, observable rep behaviour.

- Difficulty should be sequenced deliberately. Start reps on Scenario 1 (Branch RM Cross-Sell, Beginner) and advance to Scenarios 3, 5, and 10 (Advanced) only after they’ve demonstrated competency at the intermediate level. Throwing a new rep into a high-stakes scope-creep or win-back conversation too early damages confidence without building skill.

- The goal is capability, not completion. A rep who completes a scenario and scores 68/100 has identified their gap. A rep who scores 68/100 ten times and never improves has a coaching conversation to have; not another scenario to complete.

Conclusion

Roleplay scenarios are only as good as the fidelity of the practice they create. A realistic buyer persona, a specific objective, clearly defined scoring moments, and a genuine pressure point in the conversation; these are what separate a scenario that changes behaviour from a scenario that ticks a training box.

The ten scenarios in this guide are designed to cover the full arc of enterprise sales across Disprz’s core verticals: banking, insurance, pharma, retail, automotive dealerships, financial services, and IT services. Each scenario includes India-specific variants for the BFSI, insurance, and pharma contexts that no other AI sales coaching platform has built at this depth.

Build them with your own buyer personas, your own product context, and your own scoring rubrics. Run them as often as your reps need; not once a quarter, but as many times as it takes for the behaviour to become instinct.

FAQs

1) What is an AI sales roleplay scenario?

An AI sales roleplay scenario is a structured simulation of a real buyer conversation; built with a defined persona, a specific call objective, and a set of scoring criteria. The AI plays the buyer role, responding dynamically to the rep’s inputs in real time. After the call, the rep receives detailed feedback on their performance against the defined scoring moments.

2) How many scenarios should an enterprise team build to start?

Start with three: one aligned to your most common everyday customer conversation (such as cross-selling or a first product pitch), one aligned to your highest-stakes or highest-emotion moment (such as a price objection, a collections call, or a compliance-sensitive pitch), and one aligned to a known weak spot in your team’s current performance data. Add scenarios as you identify additional patterns.

3) How are AI sales roleplay scenarios different from scripted e-learning?

Scripted e-learning presents a buyer who follows a pre-written decision tree. If the rep says the right thing, the buyer proceeds positively. AI sales roleplay uses a generative AI buyer who adapts dynamically to anything the rep says; introducing unexpected objections, following up on weak answers, and behaving inconsistently when the rep tries to follow a script. This is what makes it genuinely difficult and genuinely useful.

4) How long should each AI roleplay scenario be?

Most effective sales roleplay scenarios run between 5 and 15 minutes. Shorter sessions (5 minutes) work well for discrete skill practice; opening hooks, objection handling. Longer sessions (15–20 minutes) are appropriate for full-call simulations like discovery or multi-stakeholder demos. Disprz Sales Coach supports session durations from 5 to 20 minutes, configurable per scenario.

5) Can AI roleplay scenarios be built in Indian languages?

Yes. Disprz Sales Coach supports vernacular persona configurations for Hindi and other regional languages; relevant for field reps in Tier-2 and Tier-3 markets, and for insurance agents whose buyers communicate primarily in regional languages. US-built AI roleplay platforms do not offer this capability at an enterprise level for Indian markets.

6) How does an AI buyer simulate a realistic insurance objection?

In Disprz Sales Coach, the insurance buyer persona is configured with a specific prior experience (e.g., a previously mis-sold ULIP), a defined emotional state (guarded, cautious), and a set of objection triggers (any claim about guaranteed returns raises her scepticism). The AI buyer’s behaviour is calibrated to these inputs and adjusts dynamically based on how the rep responds; becoming more open if the rep demonstrates empathy and knowledge, more resistant if they push product prematurely.

7) How do managers use scenario data to coach their teams?

The Disprz Sales Coach manager dashboard shows readiness scores by scenario and by rep. Managers can see which reps have practised which scenarios, their score trends across sessions, and the specific scoring moments where their team consistently underperforms. This gives managers focused coaching conversation starters; instead of ‘how do you think your calls are going?’ they can say ‘your objection handling score is 52/100 on the procurement scenario; let’s talk about what’s happening at the 03:00 mark.’

8) What is the IRDAI compliance sub-score in insurance scenarios?

For insurance agent training scenarios, Disprz Sales Coach includes an IRDAI compliance sub-score that flags any rep behaviour that would constitute a regulatory violation: guaranteed return claims, misleading comparisons to fixed deposits, failure to disclose key exclusions, or any language that could be classified as mis-selling. This sub-score is tracked separately from the sales performance score and triggers an escalation review if it falls below the set threshold.

View More Resources

View More Resources